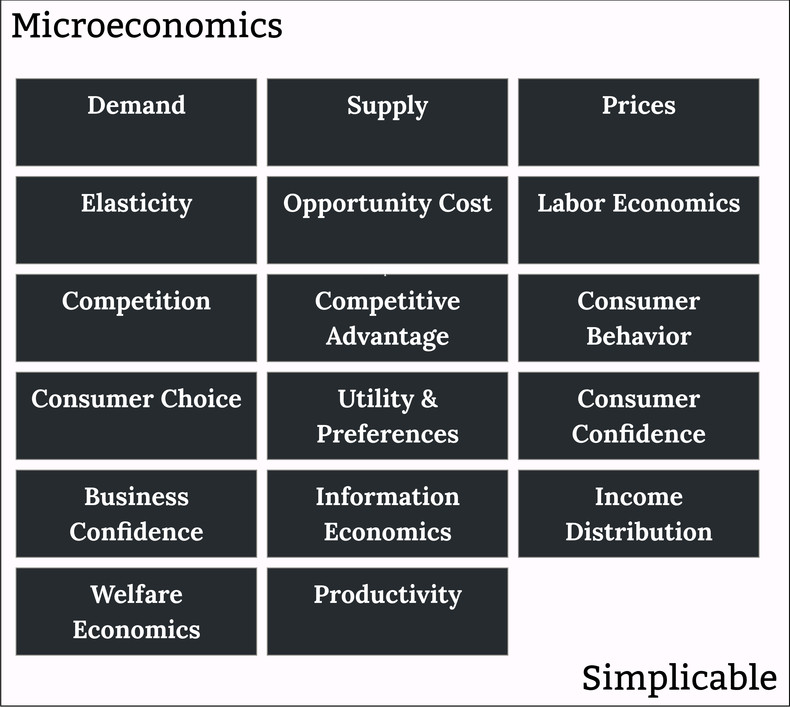

Demand

How demand for goods is influenced by income, preferences, prices and other factors such as expectations.Supply

How producers decide to enter markets, scale production and exit markets.Prices

How individuals, households and firms react to prices and influence prices with their supply and demand. For example, the observation that some customary prices appear to be sticky in that consumers resist buying above a particular historically established price.Elasticity

Elasticity is how supply and demand reacts to change. For example, a household that demands less of a good when the price increases due to the availability of substitutes.Opportunity Cost

The tradeoffs that individuals and firms make to manage constrained resources such as time, money, capital and land. For example, an individual who can choose to go to university or start a company who doesn't have enough time or money to do both.Labor Economics

Modeling the supply and demand for labor. For example, looking at how expectations for economic growth impact the labour participation rate.Competition

Modeling competition in markets. For example, the use of game theory to model a price war between competitors.Competitive Advantage

Competitive advantage is the ability of certain firms to outcompete all competition in a particular area. For example, a sporting goods company with superior brand recognition and a positive brand image that can charge premium prices and still enjoy high demand for its products.Consumer Choice

How needs, perceptions and information shape consumer choices. For example, the idea that consumers maximize their expected utility of purchases meaning that they buy the things they expect to be most useful to them.Utility & Preferences

Modeling the value of goods and services in terms of utility to consumers and consumer preferences.Consumer Confidence

How consumer expectations for the future influence spending, saving, investment and labor participation.Business Confidence

How producer expectations for the future influence hiring, capital investment and supply.Information Economics

In many cases, macroeconomics assumes that all market participants have perfect information in order to simplify models. Microeconomics may look at the realities of imperfect information and its influence on markets. For example, how uncertainty regarding product quality impacts consumer decisions.Welfare Economics

Modeling the impact of social programs on economic decisions such as labor participation or risk taking. For example, looking at how a social safety net encourages individuals to start or fund brave new businesses.Productivity

Modeling the productivity of individuals and firms including factors such as automation, tools and knowledge.Summary

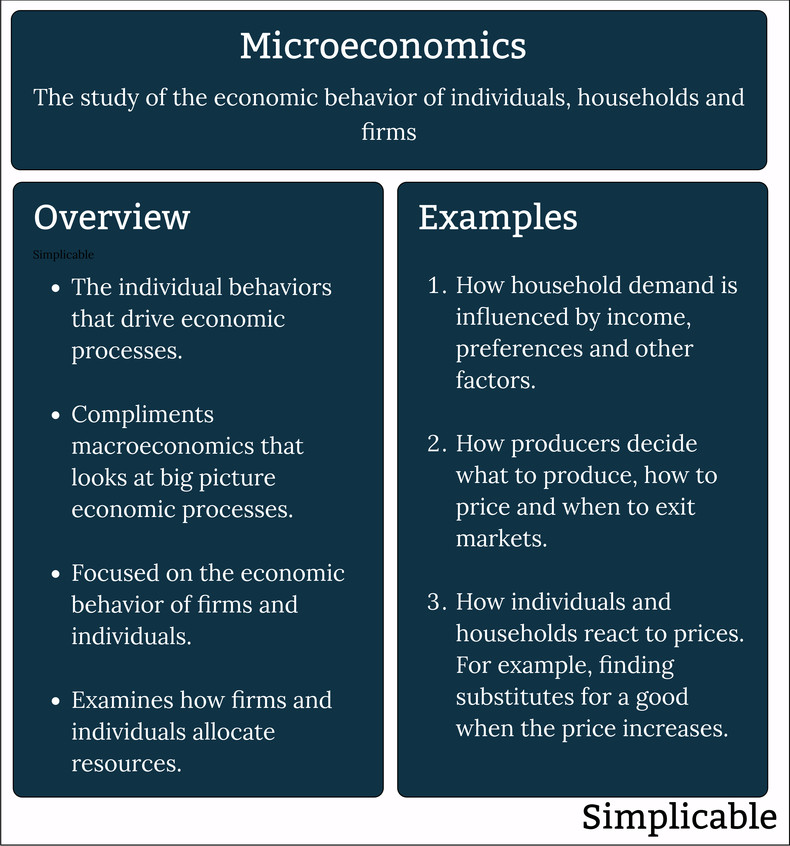

Overview

Microeconomics looks at the economic behavior of firms and individuals.

| Overview: Microeconomics | ||

Type | ||

Definition | The study of the economic behavior of individuals, households and firms. | |

Related Concepts | ||